Gender pension gaps: structural inequalities

France’s 2010 pension reform specifies that one goal of the pension system is to reduce the gender pension gap. Whereas pension disparities are usually studied in terms of the average gap, INED senior researcher Carole Bonnet and INED-associated researchers Dominique Meurs and Benoit Rapoport applied a different approach, looking instead at pension levels by whether retirees had worked in the public or private sector, as those sectors have their own pension systems, called “regimes.” Analyses of data from the “Inter-regime Retiree Sample” (EIR) run by France’s health and labor statistics department (DREES) bring to light considerably wider gender gaps in the private sector for pensions all along the income scale.

Greater disparities in the private than the public sector

Male-female retirement pension gaps are much wider for private-sector retirees than their public sector counterparts, at all points on the wage-income distribution. Average pensions for women in the private sector come to slightly over half of what they are for men, as against an average of 80% in the civil service. This is because public-sector women retirees have had less fragmented careers than women working in the private sector, and career interruptions are not as heavily penalized in the public sector when it comes to the reference wage on which the pension amount is based. The fact that women are overrepresented in the country’s civil service may be due in part to the relative advantages of public over private-sector employment.

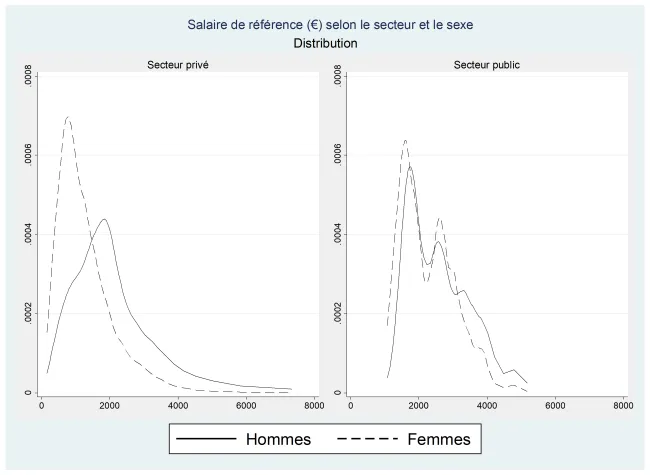

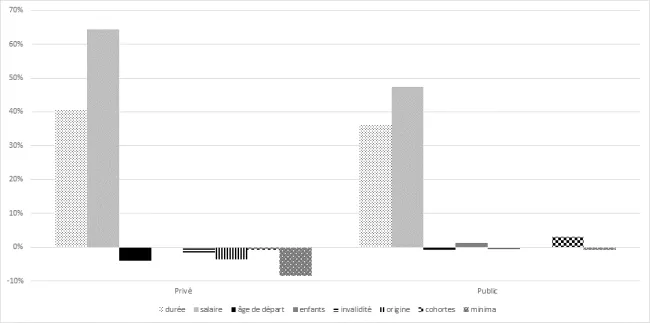

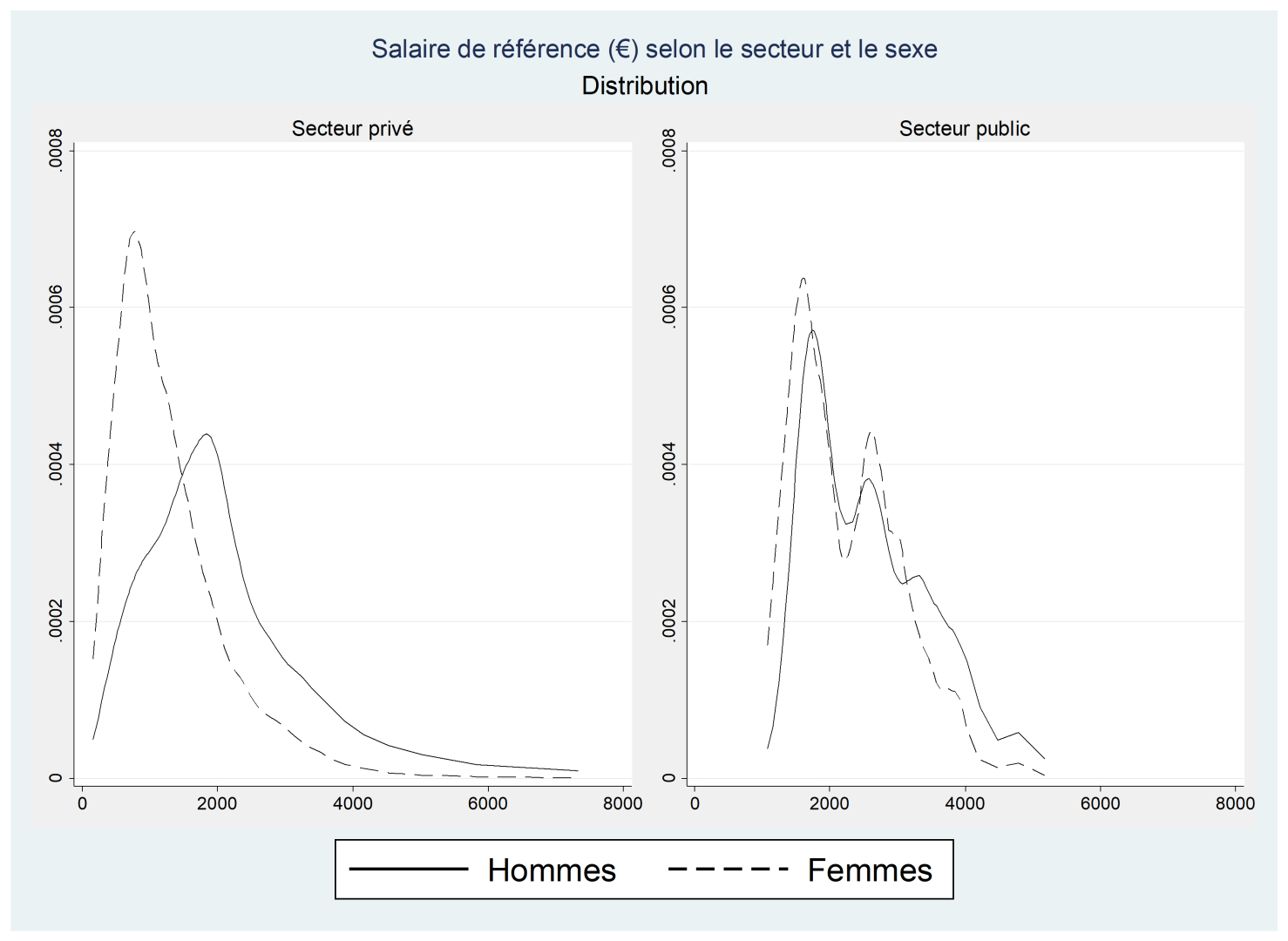

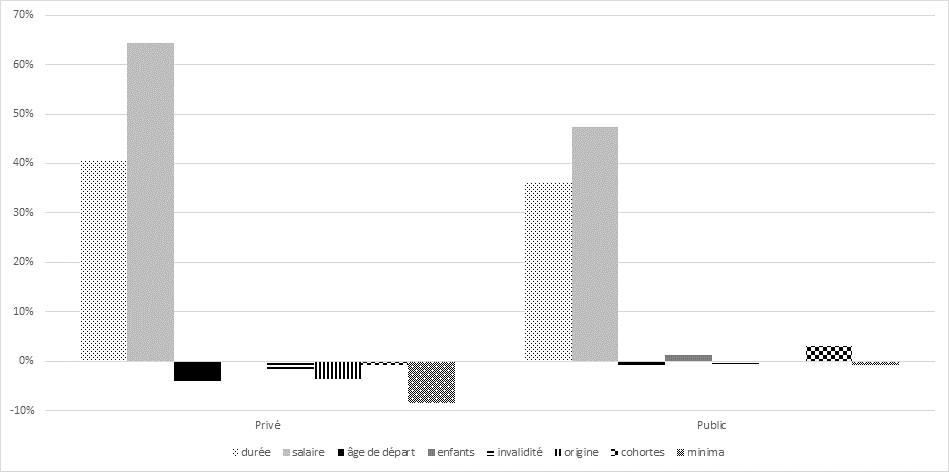

To better understand sector differences, the researchers broke down pension gaps into their variable components to identify explanatory factors. Regardless of sector, wage differences are the main factor explaining male-female pension disparities (Figure 1). Next comes length of time or periods during which the employee paid social security contributions into the pension system. The effect of this second factor is stronger in the private than in the public sector (Figure 2).

France’s minimum contributory pensions play a stronger compensatory role in the private than the public sector

Minimum contributory pensions play a major role in France when it comes to containing the male-female pension gap, especially in the private sector, where they reduce the average gap by nearly 8% (Figure 2). Without this guarantee, the private-sector gender pension gap would be even wider, particularly at the bottom of the wage scale. In the public sector, meanwhile, the minimum pension’s role in reducing the gender gap is negligible (Figure 2). Women’s careers in that sector are relatively similar to their male counterparts’, though with less access to high positions.

Gender pension gaps have different causes at the top and bottom of the pension distribution scale

The gender pension gap varies by pension level, especially in the private sector. For low-income employees, this form of gender inequality is due primarily to differences in total amount of time the employee paid social security contributions. As pension levels rise that effect gradually weakens. The gender pension gap at the highest pension levels is due primarily to reference-wage differences. However, that effect is still not as strong in the public sector due to more homogeneous work trajectories in that sector and the fact that bonuses—more often awarded to civil servants in male-dominated jobs—are not considered in determining civil service pension levels.

Figure 1 – Distribution of reference wages by sex and sector type

Figure 2 – Contributions of components to the gender pension gap explained by sector type

{kind=link}

{kind=link}

About the EIR database

Échantillon Inter-régimes de Retraités [Inter-regime sample of retirees]

The DREES [Department of research, impact studies, evaluation, and statistics] has been compiling a French administrative database called EIR since 1997. With these data on an anonymous sample representative of the entire retiree population in France, researchers can synthesize information on individuals whose pensions are paid out by the different mandatory pension regimes and so calculate total pensions. The EIR also collects the information used to calculate pensions: social security contribution periods, pension rates, individual’s situation upon retiring, pension rate increases and reductions due to deferred or early retirement, reference wages, etc. EIR 2012 was designed to represent the population aged 35 and over on December 31, 2012. Nearly all pension regimes participate in the database, with the exception of a few small mandatory supplementary pension regimes. Altogether, the sample comprises 109,966 private-sector plus 19,485 public-sector male retirees or 84.5% of all male retirees in 2012 and 113,665 private-sector plus 31,383 public-sector female retirees or 94.0% of all female retirees in 2012.

Referens

Bonnet, Carole, Dominique Meurs et Benoît Rapoport. 2020. « Gender Pension Gaps along the Distribution: An Application to the French Case » Journal of Pension Economics & Finance.